Every year more brands test cans, cartons, and PET. At the same time, glass factories still run at full capacity. So the real question is not “glass or not”, but where each format fits best.

Glass packaging is unlikely to be completely replaced in the near term. PET, aluminum, and cartons win on weight and convenience, but glass still leads on taste neutrality, high-temperature tolerance, very long shelf life potential, and strong circular recycling in well-managed collection systems.

This article breaks the decision into four practical questions:

1) where alternatives outperform glass

2) what keeps glass competitive

3) how weight, cost, and breakage shape format choice

4) which regulations and brand signals still anchor whole categories in glass

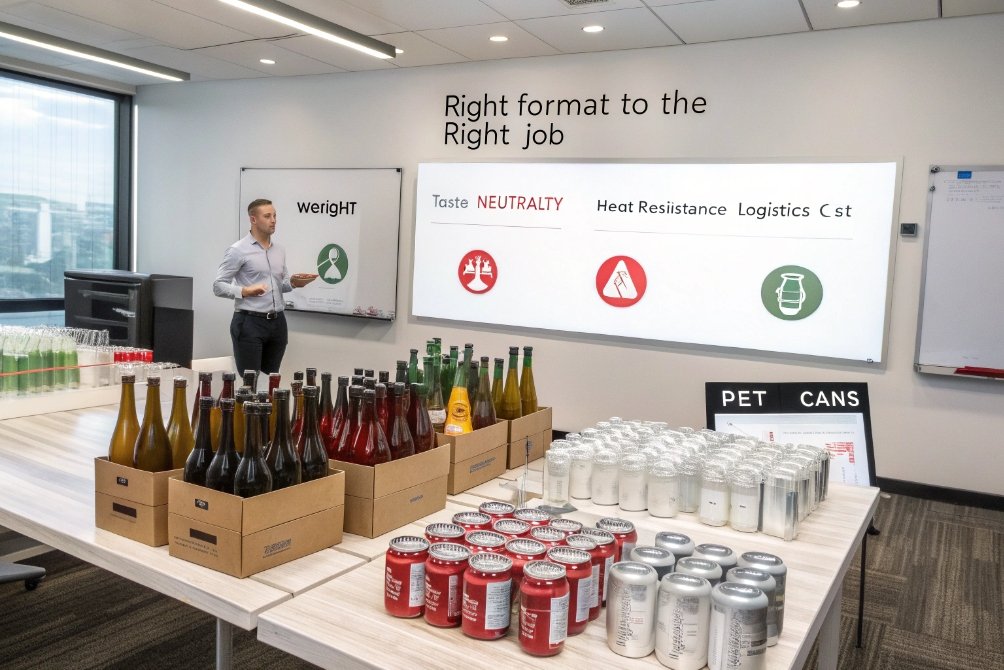

Where do PET, aluminum, and cartons outperform glass?

Glass feels premium and solid. But for many supply chains it is heavy, fragile, and expensive to move. That is where lighter formats win.

PET, aluminum, and cartons outperform glass mainly on weight, shatter resistance, logistics cost, and on-the-go convenience—especially for short shelf life, single-serve, and value products.

PET: light, tough, and “good enough” for short life

PET bottles deliver clear operational wins:

- Much lower transport weight per liter

- Lower breakage losses

- Safer use in venues that ban glass (pools, stadiums, airlines)

Modern barrier PET options—especially oxygen scavenger coatings for PET bottles 1—can improve oxygen protection enough for many juices, RTDs, and short-life wines.

But PET is still more permeable than glass, so very long storage and aroma-sensitive products can be higher risk over years.

Aluminum cans: fast, light, and fully light-blocking

Cans are ultra-light, chill quickly, and run efficiently on high-speed lines. The metal wall blocks light completely.

Cans usually win when:

- Single-serve formats matter (250–375 ml wine, cocktails, RTDs)

- Convenience and chilling speed drive demand

- Shipping distance and freight cost dominate

Trade-offs:

- Cans rely on internal polymer liners in aluminum beverage cans 2 to prevent corrosion and off-flavor. Liner selection and compatibility testing matter.

- Regulations and market preferences around liner chemistry can affect brand decisions.

Cartons and bag-in-box: cube efficiency and low breakage

Cartons and bag-in-box win hard on:

- Low packaging weight per liter

- Excellent cube efficiency in transport and storage

- Low breakage and good post-opening life for daily drinking

Trade-offs:

- Oxygen ingress through seals and polymer layers is generally higher than glass; performance varies by film structure and handling, as shown in the Comparative Study of Bag-In-Box and PET Packaging 3.

- Unopened shelf life for quality-sensitive products is often managed in months, not decades.

Bottom line: alternatives shine on logistics and convenience when the product doesn’t need extreme shelf life, heat processing, or very tight flavor protection.

What keeps glass competitive on taste neutrality and circularity?

Glass is one of the rare packaging materials that is both high-barrier and largely inert for most beverages.

Glass stays competitive because it is chemically stable, essentially gas-tight in normal use, tolerates hot-fill/pasteurization/retort conditions better than many plastics, and can be recycled repeatedly when collection and sorting are strong.

Taste neutrality and chemical stability

For wine, spirits, sauces, and sensitive beverages, the package ideally should not:

- add flavor

- remove aroma compounds

- change over time under heat/light exposure

Glass offers:

- very low interaction with contents in normal beverage conditions (see the Glass Food Contact Materials Guideline 4)

- no reliance on internal barrier liners for basic chemical protection

- stable performance for long storage windows

By contrast, many alternatives rely on layered structures and liners. These can work extremely well—but they introduce more variables (materials, adhesives, coatings, process windows, migration compatibility, aging under heat).

Heat tolerance and barrier performance

Many filling and process steps can reach 85–130 °C (depending on the product and method).

Glass generally tolerates these conditions without softening or losing shape, while plastics often require specialty grades and careful process control.

On gas barrier:

- Glass is a near-zero oxygen and moisture transmission wall.

- PET/cartons must use barrier layers or scavengers to approach that performance.

For long-term aroma stability, this difference still matters.

Circularity depends on the system

Glass can be recycled repeatedly with minimal loss of material performance when collection and sorting are strong—see the Glass Hallmark 5 and practical notes in Glass Recycling Facts 6.

Plastics can be recycled too, but real-world loops vary by region and by format (clear vs colored, mono vs multi-layer).

So “best” sustainability isn’t one universal answer—it depends on local recycling infrastructure, transport distance, and reuse/return systems.

How do weight, cost, and breakage shape the choice?

Even when glass is technically ideal, it still must pass business reality.

Glass is heavy and breakable, so it increases transport cost and breakage risk—especially in long or complex supply chains. Lightweighting and better secondary packaging reduce the penalty, but usually don’t erase it.

Weight and logistics

Rough packaging mass comparisons (order-of-magnitude):

- Heavy wine bottle: ~500–800 g

- Lightweight wine bottle: ~350–420 g

- PET: often tens of grams per liter-equivalent

- Carton: often even lower packaging mass per liter

Those differences become:

- higher freight cost per filled unit

- higher fuel use for long routes

- higher handling effort and break risk

True cost includes damage cost

Cost is not just “bottle price.” It also includes:

- line breakage and downtime

- transit losses

- extra protective packaging (dividers, heavier cartons)

- retail breakage risk and safety controls

Glass can be optimized through:

- lightweighting with controlled wall distribution

- improved annealing and coatings (lower scuff → fewer cracks)

- smarter dividers and pallet patterns

Still, in pure logistics economics, PET and cartons usually stay advantaged for low-margin volume products.

Where glass still makes financial sense

Glass can remain the best value when:

- product value is high (pack is a smaller share of retail price)

- long shelf life and flavor protection are non-negotiable

- premium cues drive pricing power

- returnable/deposit systems allow multiple trips per bottle

Are regulations and brand cues pushing brands to stay with glass?

Even when alternatives work, many brands hesitate—partly because of standards, partly because of consumer expectations.

Regulations, established quality norms, and premium positioning (especially in wine, spirits, and pharma) keep glass as the default in many categories—while sustainability pressure often pushes “better glass” (lighter, higher cullet, lower-emission) rather than a full switch away.

Regulatory anchors

In some categories, glass is the easiest compliance path because it is familiar, proven, and widely accepted:

- pharma and high-sensitivity products often use strict primary-packaging requirements

- many food systems favor low-migration, well-characterized materials

- deposit and collection rules (including targets under the Single-Use Plastics Directive (EU) 2019/904 7) shape beverage-format economics

Alternatives can qualify—but may require more validation, longer timelines, or tighter controls.

Brand signals and consumer expectations

In many markets:

- glass = heritage, quality, aging potential

- non-glass formats = convenience, value, modernity

A format change can affect:

- perceived price tier

- consumer trust

- trade acceptance (restaurants, specialty retail, collectors)

Because of this, many brands choose a portfolio strategy:

- keep glass for premium/core lines

- use cans/cartons/PET for on-the-go, entry-level, or channel-specific needs

- reduce glass impact via lightweighting + higher cullet + better logistics

Conclusion

No single material can fully replace glass across all beverages and markets. PET, aluminum, and cartons will keep growing where weight, cost, and convenience dominate. Glass will stay strong where taste neutrality, heat tolerance, long shelf life, and premium cues still decide the outcome.

The winning strategy for most brands is not “replace glass,” but “assign each format to the job it does best.”

Footnotes

-

Explains how oxygen-scavenging coatings reduce oxygen ingress and extend PET shelf life. ↩︎ ↩

-

Overview of food packaging materials, including why metal cans use internal coatings/liners. ↩︎ ↩

-

Data-driven comparison of oxygen ingress behavior in bag-in-box and PET packaging formats. ↩︎ ↩

-

Practical guidance on glass inertness and food-contact safety documentation for packaging teams. ↩︎ ↩

-

Quick summary of glass’s core performance traits, including recyclability and material stability. ↩︎ ↩

-

Clear, consumer-friendly facts about how glass recycling works and why cullet quality matters. ↩︎ ↩

-

Official EU legal text shaping collection targets that often drive deposit-return system decisions. ↩︎ ↩